Introduction

A finance charge represents the cost of borrowing money or using credit. Whether you use a credit card issued by Visa or take a loan from a bank like JPMorgan Chase, lenders apply finance charges as compensation for extending credit. These charges include interest, fees, and other costs tied to borrowing. Understanding how finance charges work helps you manage debt effectively and avoid unnecessary expenses.

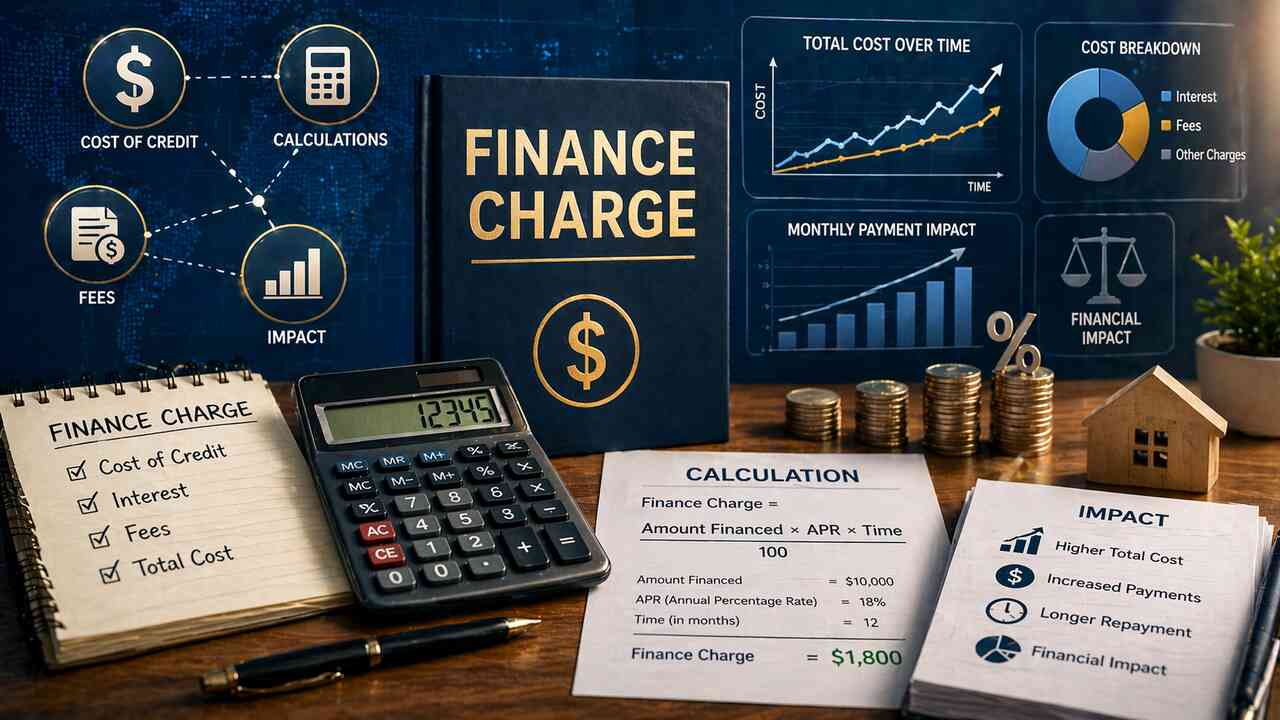

Identify Components Included in a Finance Charge

A finance charge includes all costs associated with borrowing money. The most common component is interest, calculated as a percentage of the outstanding balance. Additional elements may include late payment fees, transaction fees, and annual account fees.

Credit providers such as Mastercard often disclose these costs in agreements, ensuring transparency for consumers. Each component contributes to the total borrowing cost, making it important to review terms carefully.

Different credit products include varying combinations of charges. Credit cards, personal loans, and mortgages all structure finance charges differently based on risk and repayment terms.

Calculate Finance Charges Using Interest Rates

Finance charges are typically calculated using an interest rate applied to the outstanding balance over a specific period. The most common rate used in consumer credit is the annual percentage rate (APR).

For example, if a lender offers a 15% APR, the finance charge accumulates based on the unpaid balance over time. Financial institutions like American Express calculate these charges daily or monthly depending on the agreement.

The calculation method affects the total cost significantly. Compounding interest increases the amount owed if balances are not paid in full, making it essential to understand how rates are applied.

Compare Finance Charges Across Credit Products

Different financial products apply finance charges in distinct ways. The table below highlights key differences:

| Credit Product | Typical Finance Charge Structure | Key Features |

|---|---|---|

| Credit Cards | Variable APR + fees | Revolving balance, flexible payments |

| Personal Loans | Fixed interest rate | Set repayment schedule |

| Mortgages | Long-term interest + fees | Lower rates, secured by property |

| Auto Loans | Fixed or variable rates | Tied to vehicle financing |

Credit cards often have higher finance charges due to flexibility, while secured loans like mortgages typically offer lower rates.

Understanding these differences helps borrowers choose the most cost-effective option for their needs.

Recognize Factors That Influence Finance Charges

Several factors determine the size of a finance charge. Credit score plays a major role, as higher scores usually result in lower interest rates. Lenders assess risk before assigning rates.

Financial institutions like HSBC consider additional factors such as loan amount, repayment period, and market conditions.

Economic trends, including inflation and central bank policies, also affect interest rates. Borrowers should monitor these factors when taking on new credit.

Reduce Finance Charges Through Smart Repayment Strategies

Reducing finance charges requires proactive financial management. Paying balances in full each month eliminates interest charges on credit cards. Making payments early reduces the average daily balance used in calculations.

Borrowers using services from Citibank or similar institutions can also benefit from lower rates by maintaining good credit and negotiating terms.

Consolidating debt into lower-interest loans is another effective strategy. These approaches minimize the total cost of borrowing over time.

Understand Legal Disclosure of Finance Charges

Regulations require lenders to clearly disclose finance charges to consumers. In many countries, laws mandate transparency through standardized terms like APR.

Organizations such as Consumer Financial Protection Bureau enforce rules ensuring borrowers understand the true cost of credit.

Loan agreements, credit card statements, and financial disclosures all include detailed breakdowns of finance charges. Reviewing these documents helps avoid unexpected costs.

Analyze the Impact of Finance Charges on Debt

Finance charges directly affect how much you repay over time. High interest rates can significantly increase the total cost of borrowing, especially for long-term loans.

For example, carrying a balance on a high-interest credit card from providers like Discover Financial Services can lead to compounding debt if payments are minimal.

Understanding this impact encourages responsible borrowing and timely repayment, reducing financial stress and long-term obligations.

Compare Fixed vs Variable Finance Charges

Finance charges can be fixed or variable depending on the credit agreement. Fixed rates remain constant throughout the loan term, providing predictable payments.

Variable rates fluctuate based on market conditions. Institutions like Barclays may adjust rates periodically, affecting monthly costs.

Choosing between fixed and variable rates depends on risk tolerance and market expectations. Fixed rates offer stability, while variable rates may provide lower initial costs.

Evaluate Finance Charges in Everyday Transactions

Finance charges are not limited to large loans. They also apply to everyday financial activities such as credit card purchases, installment plans, and deferred payment options.

Digital payment platforms like PayPal may include finance charges for certain credit services or installment payments.

Understanding how these charges apply in daily transactions helps consumers make informed financial decisions and avoid unnecessary costs.

Identify Common Fees Included in Finance Charges

Finance charges often include various fees beyond interest. These may include:

| Fee Type | Description |

|---|---|

| Late Payment Fee | Charged for missing due dates |

| Annual Fee | Yearly cost for maintaining an account |

| Balance Transfer Fee | Cost for moving debt between accounts |

| Cash Advance Fee | Charged for withdrawing cash via credit |

Each fee adds to the total cost of borrowing, making it essential to review terms before using credit.

Conclusion

A finance charge is the total cost of borrowing money, including interest and additional fees. It applies to various financial products, from credit cards to long-term loans, and significantly impacts the total repayment amount.

By understanding how finance charges are calculated, what factors influence them, and how to reduce them, borrowers can make smarter financial decisions. Managing finance charges effectively leads to lower debt costs and improved financial stability.

Read Also: How Many Jobs Are Available in Finance? A Complete Market Overview